Why would a sweet, charming, seemingly docile pooch like this need animal liability insurance?

Well, because even the most well-behaved dog can get into trouble.

Picture this: You’re in a rented, fully furnished apartment, and your beloved Labrador, excited to see you, boisterously bounces around the room, destroying the landlord’s furniture as she goes.

Or perhaps your rented apartment is unfurnished and your darling dog scratches your bedroom door every morning to get you out of bed. Two weeks in and the door’s a wreck.

Or maybe you’re walking your Labrador along the sidewalk when she escapes, darts into the road, and causes an accident.

Who is liable in these situations? The answer could be you, so maybe it’s time to think about animal liability insurance.

This article sets out the facts on animal liability insurance and suggests ways in which PetScreening can help landlords, pet owners, and renters navigate these types of policies.

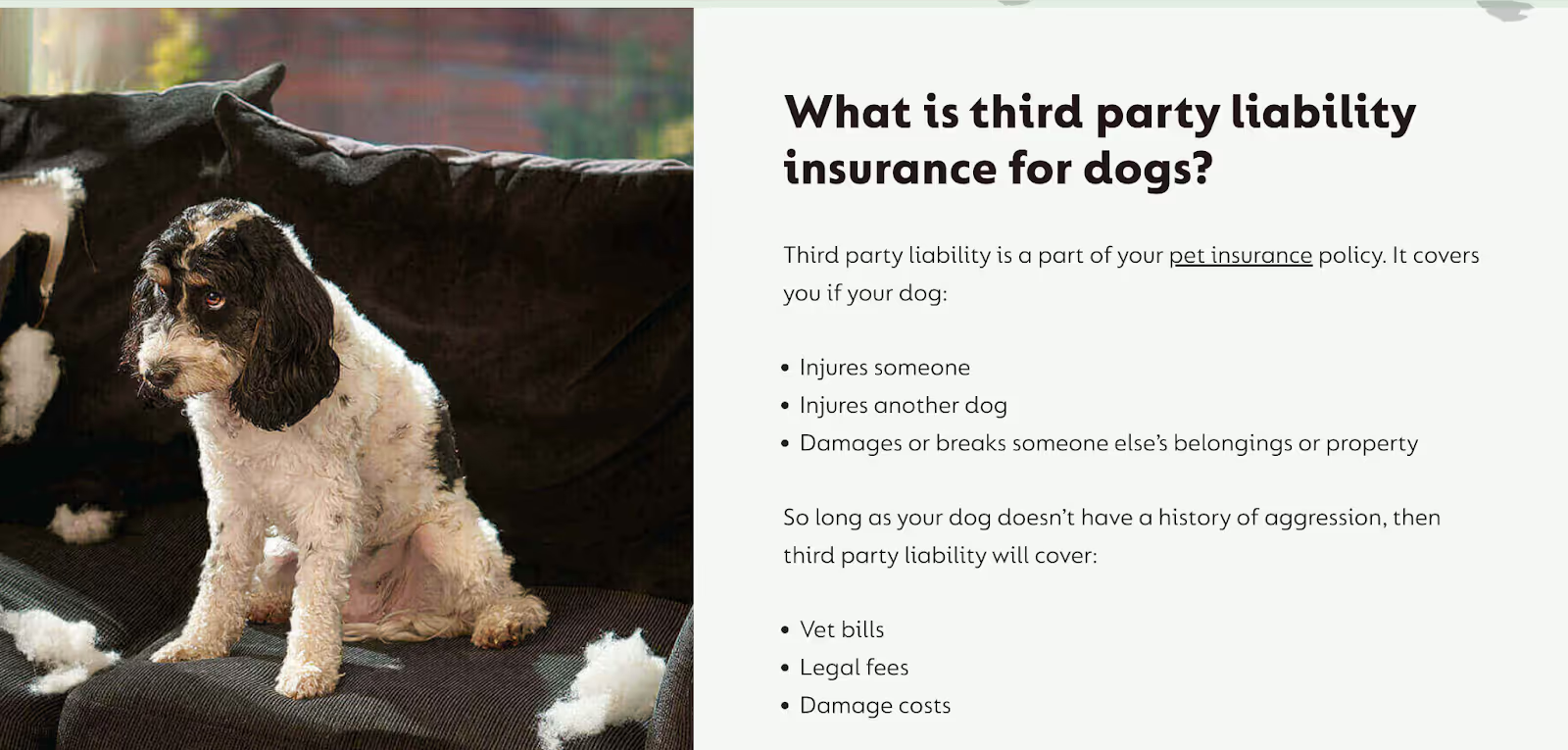

Animal liability insurance is a form of third party insurance coverage that would cover damages to another person, (like medical bills) or to their property (like furniture or carpeting). [It differs from simple pet insurance, which typically only covers the health concerns of your pet and associated vets’ fees. Animal liability insurance, on the other hand, will cover the costs of damage and injury to third parties or their property by your pet. Quite often, animal liability insurance is offered as an add-on to pet vet insurance, but if you want it, you must make sure it’s included in your policy.]

Animals can be unpredictable, causing damage and harm. Animal liability saves you from potentially paying thousands of dollars to someone impacted by your pet.

For example, 85% of landlords have experienced property damage by pets. And while it’s true that landlords have to deal with significant damage from people, pets don’t pay the rent and not everyone who rents has a pet. It makes sense that landlords are cautious about renting to pet owners.

The American Veterinary Medical Association reports that there are approximately 4.5 million dog bites in the US every year. And on average, a dog attack with more than minor injuries has a payout between $30,000-$50,000. Animal liability insurance offers the pet owner financial safety when these unexpected events occur.

Animal liability insurance is designed to cover all these situations.

It covers liability to third parties for:

[In most cases, animal liability insurance will include cover for these eventualities, together with associated legal fees.]

If you’re a homeowner, you may find that a certain amount of animal liability insurance is included in your homeowner’s insurance policy. But it may be quite limited in scope and only confer coverage up to a low amount.

Equally important, it is only likely to cover dogs and not other pets, such as cats, which can also cause damage.

Likewise, only comprehensive car insurance covers car accidents caused by animals, yours and those outside of your vehicle.

If you rent property from a landlord, you will not automatically have animal liability insurance (unless your landlord provides it, which is unlikely, and the premium costs would probably be added to the cost of the rent).

In this situation, animal liability insurance might be a condition of the rental agreement; but in any event, this insurance is essential to protect renters against claims by landlords against damage done by their animals.

[The chart above shows the number of dogs with pet insurance in the US. While some pet insurance policies include animal liability insurance coverage, not all do. If you want animal liability insurance, you must ask for it, and you must also double-check that the terms of your policy are sufficient for your purposes.]

If you are a homeowner, you might feel that the animal liability coverage in your household insurance is sufficient.

But think again. There is a considerable potential liability to think about. Taking out independent animal liability insurance might give you the following:

If you’re a renter, the advantages of a renters insurance policy are even more clear. Taking out independent or additional animal liability insurance could lead to:

Coverage typically includes veterinary bills, medical expenses, legal fees, and costs to repair damage.

And if you are a landlord who wants to protect their property and rent to pet owners, consider making animal liability insurance part of the rental agreement.

Please note that this article is for general information and is meant as a starting point only. It does not comprise legal advice. Also, remember that every animal liability insurance policy is different. You MUST read your policy’s small print carefully, including the policy limits, to ensure it gives you the coverage you need.

Subject always to the terms of the policy, third-party animal liability insurance may give you coverage if your dog bites a person or another dog. Dog bites are a serious business [as is clear from the statistics quoted earlier in this article].

Breed and temperament are important here, so you should pay attention to breed lists. If your dog is of a particularly aggressive breed or temperament, then animal liability insurance may not apply. Always give full and honest disclosure to your insurers (otherwise, the insurance may be invalidated) and seek their advice about the best breeds to own in your particular circumstance.

Dogs on the road can be as lethal as a speeding motorist.

So, like a speeding motorist, you should have third-party insurance for your dog. If your dog causes an accident, the person involved might need medical attention for bodily injury, and third-party liability insurance can cover you for:

So, can you see how important third-party animal liability insurance is?

But it will also cover you for less obvious types of accidents. For instance, consider the following scenarios:

Third-party animal liability insurance could cover you.

Third-party animal liability insurance could cover you.

Believe it or not, the customer might have a claim for not just the cost of the steak but also loss of enjoyment.

Animal liability insurance might cover you on this as well.

Dogs can damage other people’s property. They can destroy fences, doors, tables, carpets, and cars, and more.

If the damaged property isn’t yours, the owner will almost certainly want to be reimbursed.

Third-party animal liability insurance should cover you for these circumstances, depending on the policy’s depth and breadth.

If you rent a property from a landlord, the landlord may not allow pets (other than, perhaps, emotional support animals and working animals) on the premises at all.

If he or she does allow pets on the property, it may only be on condition that you have third-party animal liability insurance for your pet(s).

What if your dog took to peeing or pooping on the carpet? Or scratching at the door? Or chewing on table legs?

A good third-party animal liability insurance policy could cover all these eventualities.

[It’s possible that renters would be required to cover not just the replacement cost of the item damaged but also consequential costs, such as freighting, the time spent by the landlord to source a replacement, and building and installation costs — together with any associated legal costs.]

If you plan on taking your dog to work, you might need an extension to your policy that covers third-party animal liability at work. In any event, you should check that your policy covers taking your dog to work.

And before you take Fluffy in for a visit, consider what would happen if your dog knocked over an expensive computer? Or destroyed a report? Or, in a moment of excitement, bit one of your coworkers who was trying to pet him or her?

If your dog is a working dog, such as a companion dog, therapy animal, emotional support animal, or guide dog, special terms may apply to your policy. You should always declare your animal’s status honestly and diligently and check that the terms of your policy cover your needs.

If you are a dog walker, you will need specialist public liability insurance to cover every eventuality, including injuring people, damaging property, and losing or injuring clients’ dogs.

There is specialist insurance available for people who train dogs. This is really beyond the scope of this article, but if you are a dog trainer, speak to your insurer to ensure that your insurance covers your needs.

Every animal owner should have health insurance in case their animal becomes sick. These types of insurance policies vary, but you should at least ensure that your insurance will cover ongoing chronic illnesses on a rolling basis.

Many pet health insurance policies for dogs include some form of third-party animal liability insurance as an add-on, but you will need to pay an enhanced premium for this coverage.

Always check that the policy you are purchasing has the coverage you need.

Your home insurance provider may provide some animal liability insurance. Although you own your own home and damage to your property will not affect a third party, you still need animal liability insurance for damage to third-party property outside the home or personal injury inside or outside the home.

Yes. If your animal damages any of the landlord’s property, then you are liable. As this article explains, there are other good reasons to have third-party animal liability insurance as well.

Very carefully. Every policy is different, and you must check that your policy’s depth and breadth give you the coverage you need. While it’s very important to read the whole policy very carefully, pay particular attention to the exclusions.

PetScreening has created the pet industry’s leading and first pet policy management software solution. This means it helps landlords control liabilities by using data more thoughtfully to understand the risk. The idea is that this will help landlords accept pets and pet owners more easily. PetScreening doesn’t offer insurance itself but helps manage liability through its software.

This can only help pet owners because, as landlords and property managers learn to quantify the relevant risks, they can offer solutions to pet owners that will make it easier for them to have pets on their rented properties.

Now you know how crucial it is for animal owners and renters to seek out appropriate animal liability insurance. If you are a renter with a pet, it’s important to find a landlord who will lease rental properties to pet owners.

If you are a landlord or an owner of commercial premises, such as an employer, you need to understand the risks of allowing renters or employees to keep animals and quantify those risks so you can properly understand their impact. It may be, for instance, that once those risks are properly understood and quantified, you might be more amenable to allowing animals on your property. And this might open up new markets for renters.

If you are a landlord or employer and are keen to know more, then contact PetScreening today.

Please note carefully that this article is for general information and should be considered a starting point only. It does not comprise legal advice. Note that every animal liability insurance policy is different. You MUST read your policy’s small print carefully, including the policy limits, to ensure it gives you the coverage you need.